Welcome to the land of pork roll, diners, and Sopranos reruns – New Jersey, where even our debt has attitude! Navigating the treacherous waters of bankruptcy-in-nj-a-path-to-financial-independence/” title=”Navigating Chapter 7 Bankruptcy in NJ: A Path to Financial Independence”>debt relief in the Garden State may seem daunting, but fear not, dear reader. From the bright lights of Atlantic City to the scenic beaches of Cape May, we’ve got the inside scoop on how to tackle your debt with a wink and a smile. So grab a slice of pizza, sit back, and let’s get ready to rock your financial world in the most Jersey way possible. fugghedaboutit!

Understanding Debt Relief Options

So, you find yourself drowning in debt, huh? Don’t worry, you’re not alone. But fear not, my financially burdened friend, for there are debt relief options out there that can help you crawl out from under that mountain of bills. Let’s explore a few of them, shall we?

First up, we have debt consolidation. This handy little trick involves lumping all of your debts into one big pile and paying them off with a single, hopefully lower, interest rate. It’s like playing a game of financial Tetris, but instead of making lines disappear, you’re making debt disappear. Sounds fun, right?

Next on the agenda is debt settlement. This involves negotiating with your creditors to lower the amount you owe. It’s like haggling at a flea market, but instead of arguing over the price of an old lamp, you’re arguing over the price of your financial freedom. It’s a high-stakes game, folks.

And last but not least, we have bankruptcy. Ah, the nuclear option of debt relief. It’s like hitting the reset button on your finances, but with a lot more paperwork and a side order of shame. But hey, sometimes desperate times call for desperate measures, am I right?

Debt Consolidation vs. Debt Settlement

So you’ve found yourself knee-deep in debt, huh? Yeah, we’ve all been there. But fear not, my friend! There are options out there to help you get out of this financial pickle.

Let’s talk about debt consolidation. It’s like a financial superhero swooping in to save the day. With debt consolidation, you can combine all your debts into one easy-to-manage monthly payment. It’s like herding cats, but instead of cats, it’s your bills. And who doesn’t love a consolidated bill, am I right?

On the other hand, we have debt settlement. Think of it as your financial fairy godmother granting your wish for lower debt. With debt settlement, you negotiate with your creditors to pay off your debts for less than what you owe. It’s like a Black Friday sale on your bills, but without the crazy crowds and long lines.

So, which option is right for you? It all depends on your financial situation and goals. Do you want to simplify your payments with debt consolidation, or do you want to save some cash with debt settlement? Either way, just know that there’s light at the end of the debt tunnel. And hey, maybe one day you’ll look back on this mess and laugh. Or cry. Or both.

Pros and Cons of Credit Counseling

So you’re thinking about diving into the wonderful world of credit counseling, huh? Well buckle up, because we’re about to break down the pros and cons for you in a way that’s as entertaining as it is informative!

Let’s start with the pros, shall we? First off, credit counseling can help you create a realistic budget and develop a plan to pay off your debts. It’s like having your very own financial fairy godmother waving her wand and making all your money problems disappear! Plus, credit counselors can negotiate with your creditors to lower interest rates and monthly payments, saving you potentially thousands of dollars in the long run. Talk about a win-win!

But of course, like everything in life, credit counseling has its downsides too. One major con is that it can impact your credit score. Sure, it might take a hit initially, but think of it as ripping off a Band-Aid – it stings at first, but it’s for the greater good in the end. Another potential downside is that some credit counseling agencies charge fees for their services. Hey, these financial wizards ain’t working for free, you know!

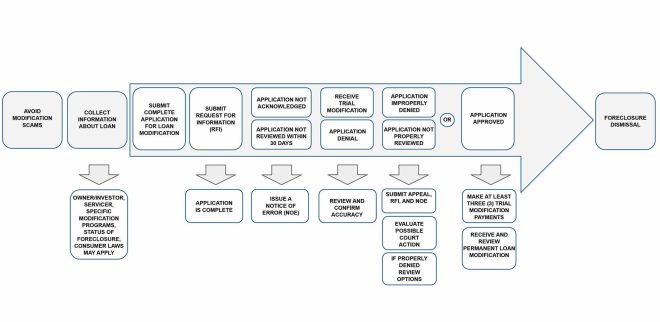

Bankruptcy: Is it the Right Choice for You?

Before you jump into declaring bankruptcy, ask yourself if it’s really the right choice for you. Sure, it might sound tempting to wipe the slate clean and start fresh, but there are a few things to consider before taking the plunge.

First off, take a good look at your financial situation. Are you drowning in debt, or just treading water? Make a list of all your debts, from student loans to credit card bills to that $20 you borrowed from your friend last week. Seeing it all laid out in front of you might make you reconsider hitting the panic button.

Next, think about the long-term consequences of bankruptcy. It might solve your immediate money problems, but it can also tarnish your credit score for years to come. Do you really want to be living off ramen noodles and watching your Netflix account get shut off because you couldn’t resist buying that new pair of shoes?

Remember, bankruptcy isn’t a magic cure-all. It’s a serious decision that can have lasting effects on your financial future. So before you make any rash decisions, take a deep breath, crunch some numbers, and maybe even talk to a financial advisor. Your future self will thank you.

Navigating New Jersey’s Debt Relief Laws

So, you find yourself drowning in debt in the Garden State, huh? Fear not, because New Jersey has some handy debt relief laws that might just save your financial bacon. Let’s take a closer look at how you can navigate these laws like a boss:

First things first, it’s important to know that New Jersey offers various options for debt relief, including bankruptcy, debt settlement, and debt consolidation. Each option has its own set of rules and regulations, so be sure to do your research before diving in headfirst. Remember, knowledge is power (and in this case, it might just save you from financial ruin).

When it comes to bankruptcy, New Jersey follows federal bankruptcy laws, but also has its own exemptions that you can take advantage of. These exemptions allow you to protect certain assets, such as your home, car, and personal property, from being seized by creditors. Pretty nifty, huh? Just make sure you brush up on these exemptions before filing for bankruptcy.

Debt settlement is another popular option for debt relief in New Jersey. This involves negotiating with your creditors to settle your debts for less than what you owe. It’s kind of like haggling at a flea market, except way more high stakes. With debt settlement, you can potentially slash your total debt and avoid bankruptcy altogether. Just be prepared to flex those negotiation muscles and sweet talk your way to financial freedom.

Avoiding Debt Relief Scams and Predatory Lenders

When it comes to dealing with debt, it can feel like you’re wading through a swamp filled with predatory lenders and shady scams at every turn. But fear not, dear reader, for I am here to be your trusty guide through these treacherous waters.

First and foremost, **always do your research** before committing to any debt relief program or lender. Look for reviews, check with the Better Business Bureau, and ask friends and family for recommendations. You wouldn’t jump off a cliff without checking to see if there was water below, would you?

Next, be sure to **avoid any company that promises quick fixes or guarantees**. If it sounds too good to be true, it probably is. Remember, Rome wasn’t built in a day, and neither will your debt be magically erased overnight.

Lastly, **trust your gut**. If something feels off or fishy about a lender or program, listen to your intuition. It’s like your spidey sense, but for financial matters. Remember, it’s better to be safe than sorry when it comes to your hard-earned money.

FAQs

How can I determine if I need debt relief in New Jersey?

Well, do you avoid checking your mailbox because you’re afraid of seeing yet another bill? Do you break out in a cold sweat every time your phone rings, fearing it’s a debt collector on the line? If you answered yes to either of these questions, it might be time to consider debt relief in New Jersey.

What are some options for debt relief in New Jersey?

There are a few options you can consider, such as debt consolidation, debt settlement, or even bankruptcy. Just remember, each option has its own pros and cons, so make sure to do your research before making a decision.

How can I find a reputable debt relief company in New Jersey?

First, ask around for recommendations. Your friends, family, or even your dog walker might have some great suggestions. Next, be sure to do some online sleuthing. Check reviews, ratings, and any complaints filed against the company. You don’t want to end up in more debt because of a shady company, right?

Will opting for debt relief in New Jersey affect my credit score?

Short answer? Yes. Long answer? It depends on the type of debt relief you choose. Debt settlement and bankruptcy can have a negative impact on your credit score, while debt consolidation might not impact it as much. But hey, sometimes you have to take a hit in the short term to improve your financial situation in the long run.

Can I negotiate with my creditors on my own for debt relief in New Jersey?

Absolutely! You can try your hand at negotiating with your creditors on your own. Just remember to be polite, persistent, and prepared. And maybe throw in a few jokes to lighten the mood. Who knows, they might just appreciate your sense of humor and cut you a deal.

Navigating Debt Relief in New Jersey: A Comedy of Errors

Congratulations on making it through the treacherous waters of debt relief in New Jersey! Remember, navigating these murky waters can be a wild ride, but with a bit of humor and determination, you’ll come out on the other side with your sanity (mostly) intact.

So, whether you’re dodging aggressive debt collectors or struggling to decipher complex financial jargon, just know that you’re not alone in this chaotic journey. Keep your chin up, hold onto your sense of humor, and remember that there’s light at the end of the tunnel – hopefully not an oncoming debt train!

Stay strong, stay savvy, and may your future be debt-free and full of financial prosperity. And hey, if all else fails, there’s always the Jersey Shore to drown your financial sorrows in a sea of spray tans and fist pumps. Happy navigating!